Startup business success comes down to effectively scaling and growing to remain competitive in today’s marketplace. This can be daunting for an entrepreneur, especially when starting out with limited resources.

In this blog, we’ll explain the difference between scaling and growing and provide actionable tactics that you can use, right away, to scale your startup and drive sustainable growth over time.

Whether it’s finding new customers, increasing visibility, or generating revenue, we’ll explore all the key components needed to take your entrepreneurial venture from a small enterprise to a successful business.

Understand the Difference Between Growth and Scaling

Growth and scaling are two different concepts that many entrepreneurs confuse or use interchangeably.

Growth is all about increasing your customer base, improving product or service offerings, or expanding into new markets to increase profitability.

Scaling, on the other hand, focuses more on optimizing processes to reduce costs while maintaining quality and service levels. The goal is to achieve greater efficiency so that growth can be maintained sustainably.

The process of scaling a startup business can include things like utilizing automation tools to streamline tasks, and investing in human resources for recruitment & training purposes.

Focus on These Main Areas for Growth & Scaling

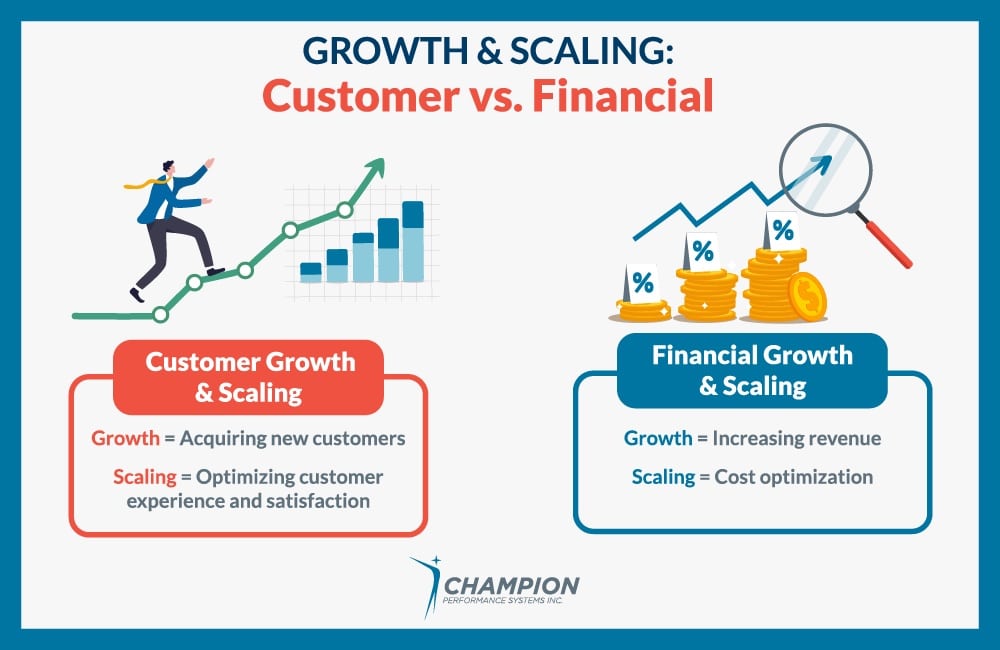

Two of the main areas businesses want to focus on growing and scaling is their customer base and increasing their revenue stream.

Customer Growth & Scaling

When it comes to customersin a startup business, growth focuses on acquiring new customers, while scaling focuses on optimizing their experience and improving satisfaction levels so that they remain loyal to your brand.

Financial Growth & Scaling

When it comes to startup business financials, growth focuses on increasing revenue through new investments or additional services/products etc.; while scaling requires focusing more on cost optimization by utilizing expense management systems and budgeting accordingly.

13 Startup Business Growth and Scaling Tactics for Progressive Entrepreneurs

There are several tactics an entrepreneur can use to grow their customer base, increase profitability, and ultimately expand their reach. Below is a list of 13 tried and true tactics that the most committed entrepreneurs use to jumpstart their business.

1. Develop a Strategic Business Plan

Developing a strategic plan for growth and scaling a startup business is essential if you want your business to reach its full potential.

Start by assessing the current state of your business and set realistic goals for the near future (6 months – 1 year). This will help you identify areas that need improvement as well as growth opportunities.

Once you have established your target goals, create an actionable plan that outlines how you are going to achieve them. While creating this plan, consider factors such as personnel hiring, technology investments and marketing initiatives.

You will also need to determine what resources are needed to implement the plan and make sure there is sufficient capital in place before taking any major steps forward.

Lastly, set up tracking systems so that progress can be monitored regularly and adjustments can be made when necessary.

2. Build a Brand Identity for Your Startup Business

A startup business needs a strong and differentiated brand identity to succeed. Your brand is much more than your logo or the colors you use on your website; it’s the sum of all of your company’s interactions with the world. Everything from the way you answer the phone, to the design of your office space, contributes to your brand identity.

As a startup, it’s especially important to establish a clear mission and set of values to guide all decision-making. Your mission should be more than just making money; it should be something that inspires both you and your team.

Once you have a mission, everything else will fall into place. From there, you can start to develop a unique brand personality and identity.

To make sure your brand identity is consistent across all channels, invest in marketing and advertising. Investing in professional design services and utilizing high-quality visuals will help to create a visual brand identity that resonates with customers. Consistent branding across your website, social media, and everywhere else, will also help build trust with potential customers.

3. Analyze Your Competition

By understanding your competitors, you can get a better insight into the market and identify opportunities or threats before they arise. It can also help inform decision-making when it comes to pricing, product/service offerings, and more.

Utilizing analytics tools such as SEO (search engine optimization) or PPC (pay-per-click) campaigns can help monitor competitor activity so you are always up to date on their strategies.

Additionally, tracking customer feedback through surveys or online reviews will provide valuable insights into how customers perceive competing brands in comparison to yours.

4. Research Automation and Technology

Automation can help streamline operational processes to increase efficiency and reduce time spent on mundane tasks. Reducing manual tasks frees up time to focus on other, more important, areas of the business.

Investing in the right technologies can also provide valuable insights into performance metrics which can help inform decisions regarding investments or hiring. Capitalizing on analytics tools will allow you to monitor progress and make adjustments accordingly.

Also consider leveraging a cloud-based system to help ensure that all employees have access to the same information regardless of their location. This eliminates any potential barriers when it comes to collaboration between teams, especially when some team members work remotely.

Utilizing automation and technology will not only improve efficiency but also create a foundation for future growth.

5. Invest in Human Resources

As your startup begins to grow and expand, you’ll want to invest in human resources to support it. This means recruiting and training the right personnel, as well as establishing a clear career development path for employees that encourages advancement within the company.

Hire and Train the Right People

Taking the right steps towards ensuring that your company has the manpower it needs is important—but human resources doesn’t stop at hiring. Taking the time to train new employees is pivotal for making sure they are properly equipped to handle their roles.

Prioritize Collaboration and Communication

Fostering a positive work culture that encourages collaboration and communication is key to keeping your employees happy and engaged with a positive work environment.

By encouraging employees to come together around shared goals, businesses can create a culture of trust that encourages innovation and problem solving which are essential components of scaling up successfully.

Creating an open communication system will ensure that every employee feels comfortable expressing their ideas, opinions or concerns – this helps break down any potential barriers between departments while also ensuring everyone is working towards the same goal.

Want to take it a step further? Investing in team-building activities such as group outings or charity events can help build relationships outside the office which can result in increased enthusiasm and productivity when back on the job!

Not sure how to get started? Human resources consulting services can provide guidance on how to properly set up your startup or success prior to growth or as it continues to advance.

6. Utilize Financial Planning

Without a clear understanding of financial statements, cash flow, capital reserves, and other key metrics, it’s impossible to accurately gauge the health of your startup business or identify potential investments or areas in need of improvement.

To ensure that you have sufficient funds available when it’s needed, budgeting correctly in advance is essential. Creating a forecast can help provide insight into future performance trends so you are better prepared for changes in revenue or expenses.

Investing in financial planning services can be beneficial if you require assistance with more complex tasks such as tax strategies or loan agreements. With the right financial plan in place entrepreneurs can set themselves up for long-term success.

7. Take Advantage of Networking Opportunities

Networking provides a platform to build relationships with other professionals that may provide valuable insights or lead to future partnerships or collaborations.

When networking, focus on actually building the relationships —not just collecting contacts.

Make genuine connections by demonstrating an interest in what others have to say and show appreciation for their time. Be open-minded about different ideas and be listening more than you are talking. Also offer assistance when possible and express gratitude whenever appropriate. It’s also a good idea to follow up after meetings with these individuals to keep the relationship alive.

By taking advantage of networking opportunities you will not only expand your knowledge base but also create an invaluable network of people who could potentially become future customers or partners.

8. Leverage the Power of Digital Marketing and Social Media

Leveraging digital marketing (such as website enhancements, blog posts and Google advertising) is an effective way to increase the visibility of your brand and establish credibility within the market.

Investing in online advertising campaigns can be incredibly beneficial for targeting specific demographics or keywords – this allows you to deliver relevant messages directly to potential customers who may be interested in your offerings.

Social media networks, like Facebook or Instagram, can be powerful tools for reaching new customers and engaging your current customers on a personal level. This helps build relationships that can result in customer loyalty over time.

By utilizing digital marketing and social media, businesses can significantly expand their reach while creating valuable connections with both current and potential customers.

9. Promote Loyalty with Customer Satisfaction and Retention Strategies

Any business, whether it’s a startup or an established corporation, will only be as successful as its ability to satisfy customers and keep them coming back for more. This is why it’s so important for growing businesses to focus on customer satisfaction and retention strategies. Here are a few key tips:

Utilize customer feedback to identify areas for improvement

The best way to find out what your customers want, and need, is to simply ask them. Make it easy for customers to provide feedback by setting up a system for collecting it regularly. Then use that feedback to make changes that will improve the customer experience.

Keep track of the progress (both the successes and failures) by utilizing data analytics tools which could reveal areas needing improvement or changes worth making. This kind of research into what works best will offer powerful insight over time.

Regularly engage with customers to build relationships and foster loyalty

It’s not enough just to provide good products and services; you also need to build relationships with your customers. Show them that you care about their experience by regularly engaging with them, whether it’s through social media, email, or in-person interactions.

Develop customer loyalty programs to reward customers for their allegiance

Customer loyalty programs are a great way to show your appreciation for your best customers. Offer rewards, like discounts or exclusive access to encourage customers to keep doing business with you.

Invest in customer service to provide exceptional experiences

Customer service is the face of your company, so it’s important to invest in making sure your team is providing exceptional experiences. Train your team members on how to properly handle customer interactions and resolve issues quickly and efficiently.

By focusing on customer satisfaction and retention strategies, you can encourage loyalty among your customer base.

10. Use Data and Analytics to Make Decisions

As a startup, it’s important to utilize data and analytics to inform your decision-making. This will help you track your performance and identify opportunities for growth.

This can include everything from analyzing customer data to tracking financial performance.

Analyzing website traffic is a great way to monitor user behavior and identify areas of improvement. Additionally, predictive analytics can be used to forecast future performance and make decisions about resource allocation.

It’s also important to monitor feedback to ensure customer satisfaction. Analyzing customer reviews or conducting surveys will help you identify areas of improvement that could increase satisfaction levels and foster loyalty over time.

11. Keep Up with Industry Trends

Investing in research and development (R&D) initiatives helps a startup keep up with industry trends. By investing in R&D, businesses can stay ahead of competitors by introducing innovative ideas or products/services that offer value to customers.

Leveraging analytics tools will help you identify areas of improvement or changes worth making when it comes to product/service offerings – this kind of research should be ongoing.

12. Monitor Progress and Make Adjustments as Necessary

If you want your startup to be successful, you need to keep a close eye on its progress. This means monitoring a variety of factors, from customer feedback to financial statements. By doing so, you can identify any potential problems and make the necessary adjustments.

One of the most important things to track is your startup’s performance against its goals. This will help you determine whether you are on track or if you need to make some changes.

You should also establish a timeline for re-evaluating your strategies. This way, you can ensure that your startup is always moving in the right direction.

13. Develop a Contingency Plan

Developing a contingency plan is essential for any business looking to take on unexpected challenges. By preparing now, you can ensure that your business will be prepared to weather any storm without putting the future of the company at risk.

Start by establishing an emergency fund in case of financial hardship; this should include savings, investments or lines of credit depending on your needs.

Create backup plans for key personnel such as managers or executives so that operations remain seamless if someone were to leave unexpectedly.

Also investing in insurance policies such as liability coverage will protect against potential legal issues down the road and provide peace of mind.

Ready to Create a Roadmap for Your Future?

The most successful startups take initiatives to grow and scale—but this is not an easy task. It requires careful planning, investments in the right tools & resources, and consistent monitoring of performance metrics.

With the right strategies in place, businesses can ensure that they are prepared to tackle their growth head on.

If you’re lost on where to start, consider investing in consulting and coaching services. This guidance can be invaluable to making progress on your journey towards a thriving enterprise.

At Champion PSI, we provide strategic business planning and guidance through a variety of coaching services. We are dedicated to helping our clients define and implement effective growth and scaling practices for their businesses.

Whether you are just launching your business or attempting a major expansion push, our strategies will give you the confidence needed to take your company to the next level.

Accelerate your startup today by scheduling a 30-minute discovery call with our licensed entrepreneur coach, Stuart Trier.

If you’re not sure which coaching speciality is right for you, contact us today at 587-897-3225 to learn more about how we can help you stay ahead of the curve with your business efforts.

: